Sustainability

The transition to sustainable business models has become essential to long‑term resilience.

Discover more

News

Limited liabilities non-financial corporates in the European Union (“EU-27”) have weathered a prolonged period of economic and geopolitical shocks over the last few years. Despite the challenging environment, characterized by the aftermath of the COVID‑19 pandemic, inflation shocks, tight monetary policies, supply chain disruptions and geopolitical tensions, European corporates highlighted a remarkable resilience, as confirmed by a broadly stable and sustainable credit risk profile between 2022 and 2024. That resilience, however, is now being tested. Corporate fundamentals remain broadly sound; however, EU-27 corporations are facing increasing pressure from tightening macroeconomic conditions and elevated geopolitical uncertainty. While negotiations between US and Iran to reach an agreement are ongoing, CRIF foresees an increase in the credit risk in the 2026-2027 period.

This is what emerges from the first edition of CRIF European Credit Outlook. By integrating default rates, proprietary scoring, financial indicators, sector trends, banking dynamics and forward-looking scenarios, the CRIF European Credit Outlook provides a comprehensive assessment of the credit risk profile of c. 48,000 limited liabilities nonfinancial corporates across the EU-27 with more than EUR 50m of revenues, positioning itself as a unique benchmark for credit risk assessment across European non-financial corporates.

"After strong revenue growth in 2022, driven by both the post-pandemic recovery and high inflation, growth rates in the European Union have gradually stabilized in 2024, averaging around 4%. However, compared to 2025 alone, the current macroeconomic environment has materially changed, primarily due to external shocks linked to the recent outbreak of conflict in the Middle East, which have had a series of effects on transportation, energy costs, and the supply chains of numerous production chains across the continent. All of this is resulting in a downward revision of growth expectations and an increase in inflation estimates for the 27 member states. A successful and sustainable agreement between US and Iran could partially improve the expectations on macroeconomic fundamentals.

For 2026, available liquidity reserves could provide some degree of mitigation against the negative impacts resulting from unfavorable geopolitical dynamics. In this sense, the commitment of EU financial institutions to supporting businesses' liquidity will be a decisive factor in addressing and managing the potential risks arising from an unstable and volatile economic environment," said Carlo Gherardi, President and CEO of CRIF. "CRIF has therefore developed advanced analytical tools enabling financial institutions and banking to integrate these emerging geopolitical risk drivers into their lending decisions, thereby supporting the sustainable financing and longterm development of the European productive system, notwithstanding ongoing global uncertainty and instability."

Adequate starting point, but early signs of strain

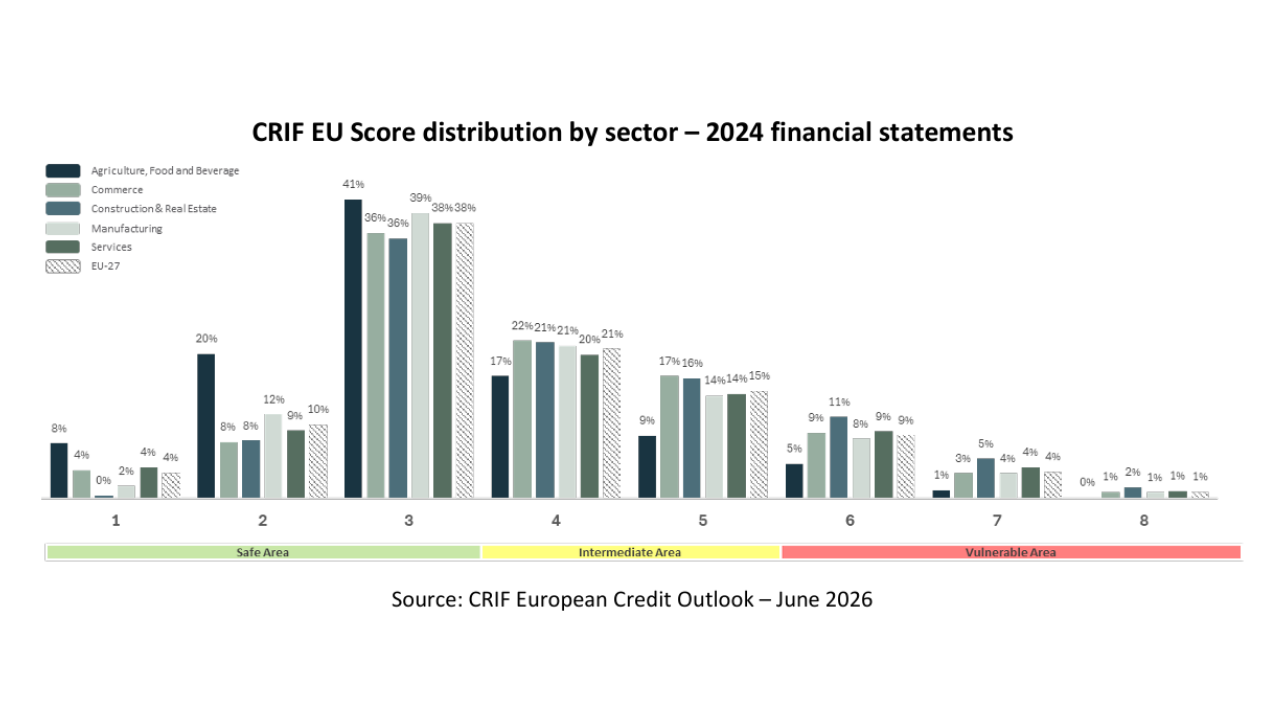

Based on the latest financial statements available, corporates in the EU-27 area have shown a broadly stable credit profile at satisfactory levels, as assessed through a proprietary CRIF scoring model (“CRIF EU Score”) designed to evaluate European firms under a standardized approach that ensures full cross-country comparability. According to the model outcome, more than half of corporates (c. 52% on average in the 2022-2024 period) fell in the “Safe” category, while only a limited share (13%) showed a “Vulnerable” credit risk. This performance reflects the ability of companies to absorb multiple shocks, from the post-pandemic effects to inflation and supply chain disruptions triggered by the war in Ukraine. The risk distribution benefitted from both the European governments’ deployment of support measures and the support of financial institutions, with the stock of outstanding loans increasing by c. 4.3% between December 2021 and December 2024, underpinning corporate liquidity which represented a key mitigating factor against the adverse effects stemming from the aforementioned adverse conditions. Loan stock levels continued to grow throughout 2025 (c.+2.4% from December 2024 to December 2025) and in the first quarter of 2026 (c. + 1.2% from December 2025 to March 2026) despite the more challenging environment.

From the economic and financial performance perspective over the 2023–2024 period, while European corporates continued to display robust liquidity profile and debt sustainability metrics, revenue growth lowered (+3.9% in 2024) coupled with an EBIT trend under pressure (-1% in 2024). The limited revenue growth recorded by European corporates in 2024 was consistent with the EU‑27 Gross Domestic Product (“GDP”) increase by around 1%, underscoring some fragilities which negatively affected, and continue to affect, the competitiveness of European players in international markets and the state of domestic demand.

Geopolitical risks are key in understanding the credit risk evolution

The historical analysis indicates that European corporates maintained, on average, a satisfactory credit risk profile, albeit within an increasingly uncertain and fragile global environment. The growing prominence of geopolitical risks is emerging as a key driver of credit risk dynamics. Current tensions in the Middle East are exerting upward pressure on energy and production input costs, as well as on supply chain reliability, contributing to expected higher inflation and economic growth under pressure for 2026. The duration of potential further disruptions to key trade routes, including the Strait of Hormuz, will be a critical determinant of inflation and GDP trends across Europe, with direct implications for the European Central Bank’s monetary policy. The CRIF baseline scenario for 2026 foresees a modest EU-27 GDP growth of 1%, a moderate rise in inflation to around 3%, and a slight increase in interest rates, under a gradual de‑escalation of the US-Iran conflict in the second half of 2026 coupled with moderately tighter credit conditions. In the event of a failure of current negotiations and new escalation of the conflict in the Middle East, the CRIF adverse scenario expects a GDP growth close to zero, an inflation rate around 5% and interest rates increasing to c. 3.5%. This could translate into more selective credit conditions, negatively affecting the financial flexibility of the most fragile European corporates.

2026-2027 Credit Outlook

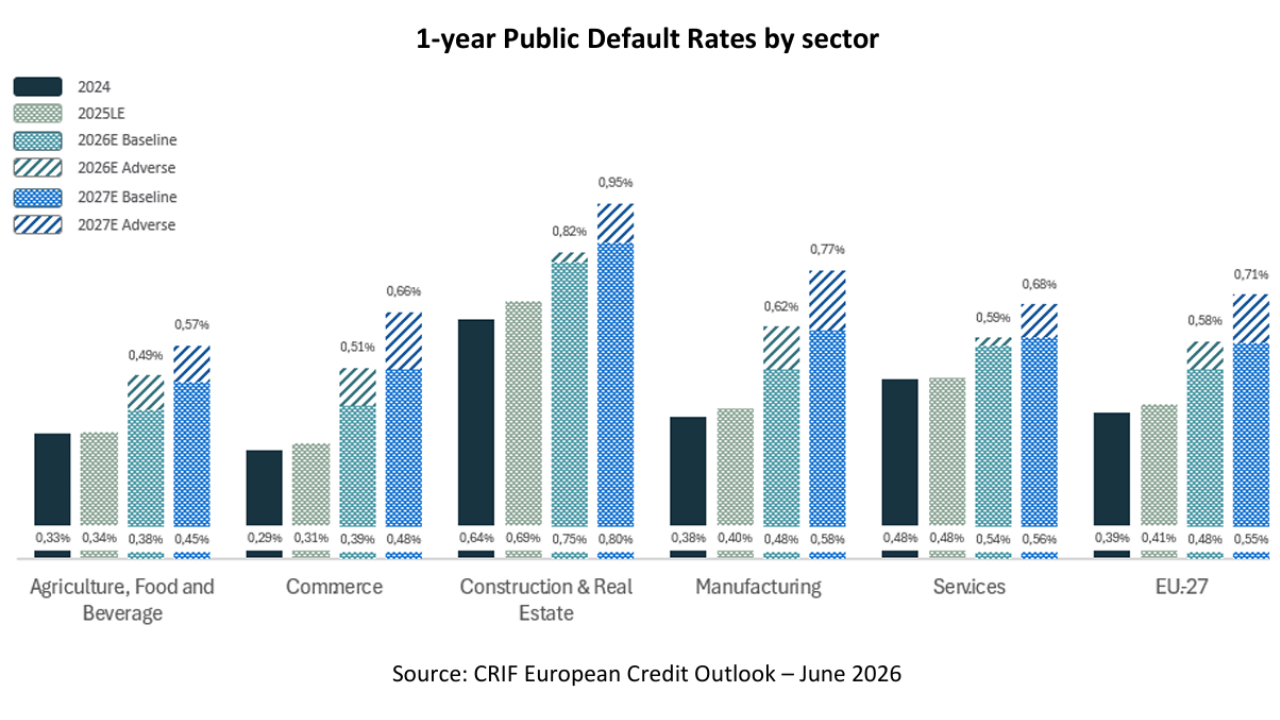

According to CRIF baseline scenario, 1-year public default rates for European corporates are expected to increase in 2026, reaching 0.48% (c. 0.4% in 2024 and 2025 according to last estimates data) whilst in CRIF adverse scenario default rates are foreseen to grow more markedly up to 0.58%. Default rates should increase further in 2027, with a more pronounced deterioration under CRIF adverse scenario. In particular, the EU‑27 default rate is forecasted at 0.55% under CRIF baseline scenario and 0.71% under CRIF adverse scenario. The 2027 outlook remains highly dependent on the evolution of macroeconomic, geopolitical and credit conditions throughout 2026. However, the trends are not homogenous by sectors.

The default rate projections also incorporate the high public debt-to-GDP ratios across the EU‑27, which would constrain European governments’ capacity to implement large-scale support measures, comparable to those deployed during the COVID‑19 crisis, without undermining fiscal sustainability. In this context, corporates’ ability to navigate the current macroeconomic and geopolitical environment will be positively influenced by the expected continued support from financial institutions. Such support is a key mitigating factor in sustaining corporates’ liquidity and managing downside risks, particularly under more adverse scenarios.

Credit risk by sector

Under the scope of the analysis, the Commerce sector represents the highest concentration of corporates with revenues exceeding EUR 50m on a statutory basis (31%), followed by Services (29%) and Manufacturing (27%), while Agriculture, Food and Beverage (7%) and Construction & Real Estate (6%) remain less relevant.

Construction & Real Estate was the most vulnerable sector with 44% of firms in the “Safe Area” (51% for EU-27) and 18% in “Vulnerable Area” (13% for EU-27) in 2024, reflecting structural exposure to cyclical demand, execution risks and production input cost volatility. Construction & Real Estate is the most vulnerable industry also in terms of default rates: 0.64% in 2024 and projected at 0.75% under CRIF baseline scenario and 0.82% under CRIF adverse scenario in 2026.

Agriculture, Food and Beverage showed the most conservative credit risk profile with c. 68% of firms in the “Safe Area”, even though the sector is exposed to multiple risk factors, including price volatility, supply chain disruptions, seasonal production patterns and weather-related shocks. By default rates, the sector showed one of the lowest historical level (0.33% in 2024), while defaults are expected to increase in 2026-2027, albeit remaining at levels below the European average.

Although the Manufacturing sector showed a risk distribution broadly aligned with the European average, financial statements operating performance indicate early signs of weakening. Manufacturing growth performance (+0.5% in 2024 vs +3.9 for EU-27) reflected an increasingly challenging operating environment. Manufacturing default rates

(0.38% in 2024) are foreseen to increase to 0.48% and 0.62% in 2026 under, respectively, CRIF baseline and adverse scenario. Commerce credit risk profile, which is characterized by the lowest default rate in 2024 (0.29%), is expected to deteriorate in 2026 with default rates forecasted to grow to 0.39% under CRIF baseline scenario and 0.51% under CRIF adverse scenario. These sectors are expected to be the most affected by the ongoing geopolitical scenario, reflecting their high exposure to international markets both as end-markets and in terms of supply chain dependencies, as well as their sensitivity to potential inflationary pressures, which would directly impact on consumers’ purchasing power.

"Over the 2022–2024 period, the EU‑27 Manufacturing sector recorded weak operating performance, reflecting intensifying competition, subdued domestic demand, adverse tariff policies from the US, and supply chain constraints. These factors negatively affected revenues and margins, coupled with persistent cost pressures and the weakness of key segments such as Automotive. Recent geopolitical developments have further exacerbated these challenges, contributing to lower global growth and higher inflation expectations. In the absence of a rapid return to normality in the Middle East conflict, most internationally exposed sectors, including Manufacturing, are likely to face increasing pressure on credit risk profile," said Luca D’Amico, CRIF Ratings CEO.

News

News

News

News

News

News

News

News

News

Would you like to unlock the full power of data & insights? Our team is here to support you.

Talk to an expert

Join over 11,000 professionals who get expert advice every week on business news and credit trends.